Student loans have recently featured in headlines. Find out what’s causing the debate, how your family might be affected, and some ways you could support students or graduates.

Choosing suitable protections to shield your family’s finances isn’t always straightforward. Weigh the pros and cons of life insurance and family income benefit.

In a bid to pass more wealth to their loved ones, a growing number of families are opening pensions for their children. Whether your child is still in nursery or already working their way up the career ladder, there could be benefits to making pension contributions on their behalf.

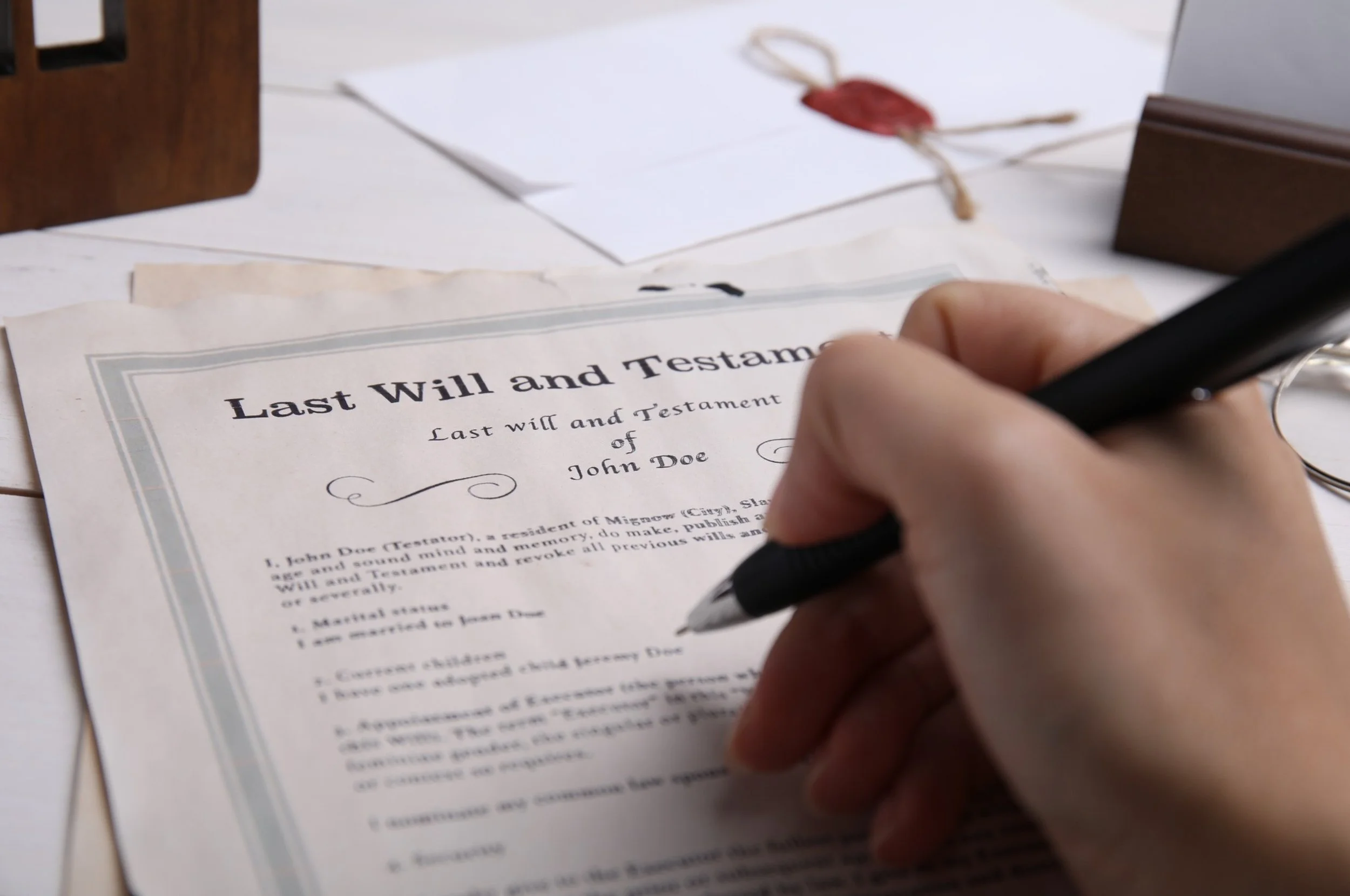

Affluent families who delay estate planning could miss out on chances to reduce a potential Inheritance Tax (IHT) bill and pass more on to their families. Find out if you could benefit from considering IHT and how you might pass on assets tax-efficiently.

Markets continued to be affected by ongoing conflict in the Middle East and technology stock volatility in June 2026. Find out what else may have affected the performance of your investments.

A hidden marginal tax rate that affects workers earning between £100,000 and £125,140 is often dubbed a “tax trap”, and research suggests it’s shaping career decisions. However, there are ways you might mitigate the additional tax charge.

Retirement is a significant life transition. Some of the financial habits that served you well during your working life might no longer suit your retirement lifestyle. Find out why.